Flutter Entertainment: When Institutions and Insiders start Accumulating

Flutter Entertainment is the world's largest online sports betting and gaming company. You will have heard of at least one of their gaming services: FanDuel, Paddy Power, Sky Betting, Betfair, Sportsbet, Skybet, Pokerstars across its four markets: UK & Ireland, Australia, International and US. It moved its primary listing to the NYSE in 2024 under the ticker $FLUT, and is now reviewing whether to delist from the London Stock Exchange entirely, with an answer due by end of June 2026.

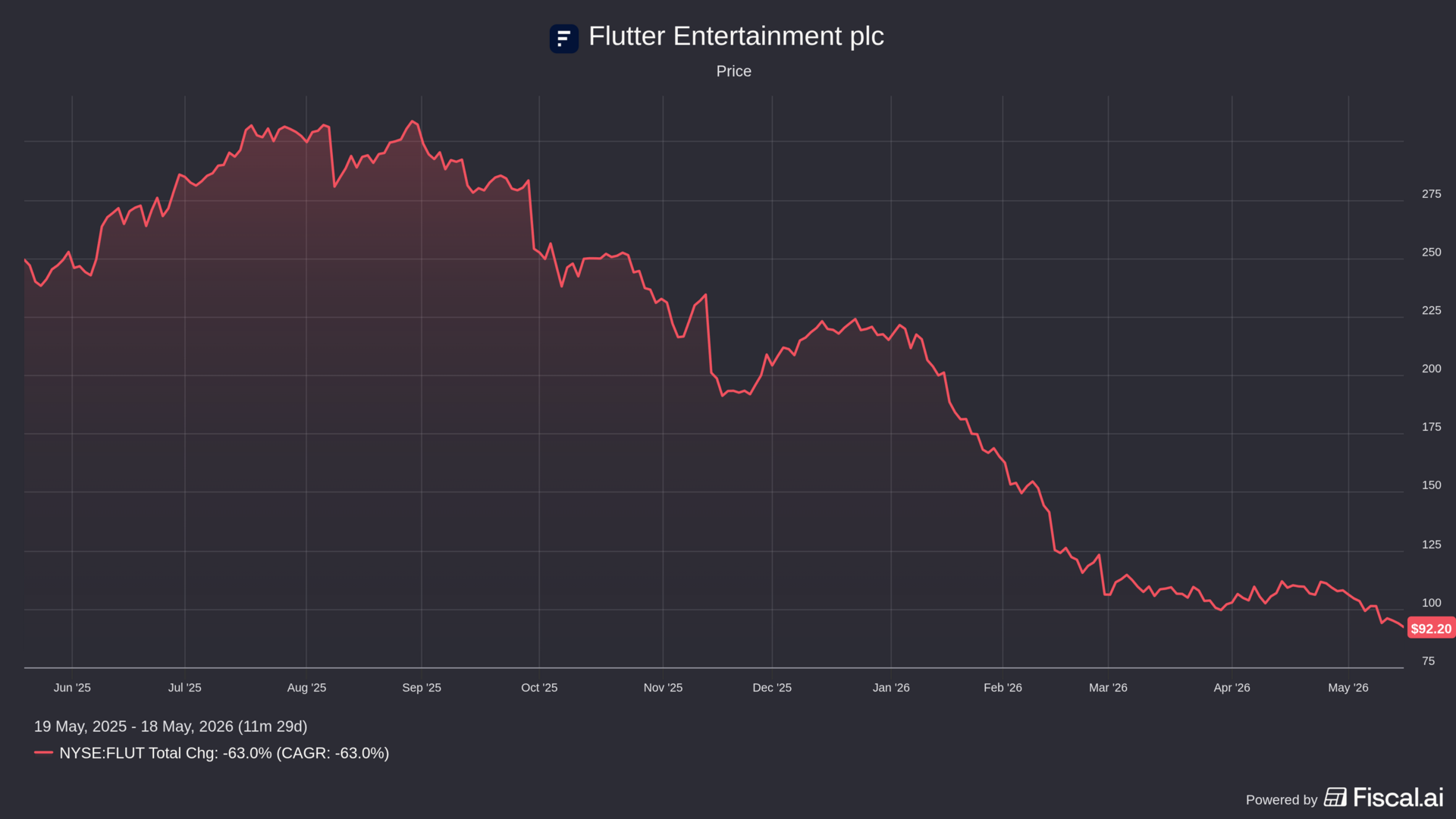

The stock is down ~63% over the past twelve months. Driven by a disappointing NFL season, margin pressure from US market investment, a UK tax increase, elevated debt, and FanDuel CEO departure announced alongside Q1 results on May 6th.

The market has priced all of that in, and then some. What it seems to be ignoring is who has been buying on the way down, how much they own, and the fact that not a single Flutter insider has made a voluntary share sale in 2026.

What Actually Matters Here

Dart has been buying constantly: Kenneth Dart (Billionaire investor and businessman) begun accumulating Flutter via total return swaps on 2nd March 2026. He has filed purchases almost every trading day since, his swap position alone stands at 15,257,655 shares as of 14th May. He also purchased 32,667,404 ordinary shares on 10th February 2026, Dart now owns over 27% of the company.

He has been adding through market volatility, bad earnings prints, and a stock sitting at a 52-week low and he's not alone. HSBC increased its Flutter position by 33,989% in Q1 2026, going from a negligible holding to 5,605,543 shares worth approximately $575M in a single quarter. BlackRock dipped below 5% in January 2026 before buying back, re-crossing the threshold on May 7th at 5.12%. Parvus Asset Management's most recent SEC filing as of March 31st shows a 6.7% stake, up from 5.1% at the start of the year. Beyond the named positions, institutional accumulation is broader, 13F filings aggregated by MarketBeat show $663M bought against $168M sold in Q1 2026 alone, with further significant increases from Millennium Management, PointState Capital, and Janus Henderson. Nearly four times as much institutional buying as selling, in a quarter where the stock hit a 52-week low.

The insider picture is cleaner than it looks: Flutter's 2026 transaction history shows sales on paper. What those sales actually represent matters, the filings for Jackson (CEO), Howe (former FanDuel CEO), Don (CLO) and Coldrake (CFO) are RSU tax withholding, shares sold automatically when restricted stock vests to cover the tax liability not open market selling.

What insiders have chosen to do with their own money continues to add further support. In the first two weeks of May alone, six separate insiders including the CLO, CEO, President of Flutter and various directors made open market purchases totaling 10,453 shares. Insiders sell for dozens of reasons: taxes, diversification, liquidity, divorce. They only buy for one.

The business model holds up better than the headlines suggest: The blanket "gambling is recession-proof" argument doesn't hold up given physical casinos took a 13% revenue hit during the 2008-2009 recession.

Flutter is however a different business. Its operations are predominantly digital: mobile sports betting, online casino, daily fantasy, across the UK, Ireland, Australia, and the US. The relevant comparison is online gambling during COVID, when physical venues closed and digital platforms saw sports betting revenue nearly quintuple between 2020 and 2022. When consumers can't or won't go out, the phone in their pocket is still there.

Geographic diversification matters here too. A slowdown in US handle growth, which has genuinely happened, doesn't collapse the whole business. FanDuel's weakness is partially offset by Sky Betting in the UK, Sportsbet in Australia, and PokerStars globally. International revenue grew 27% in Q1, driven by the Snai and Betnacional acquisitions. The US is 41% of group revenue, not all of it.

Flutter is also mid-way through a $5bn share buyback program. $1.31B has already been returned to shareholders, this is not the capital allocation decision of a management team that thinks the business is structurally impaired.

The Risks

The Q1 2026 numbers, reported May 6th per the SEC 10-Q filing, need to be read carefully. The headline figures look reasonable; group revenue up 17% YoY to $4.3B, net income attributable to shareholders of $218M. The operating picture is less comfortable; Operating profit, the measure of what the business actually earned before interest, tax, and accounting adjustments, collapsed 65% YoY from $223M to $79M. The $218M net income figure is only possible because a $293M non-cash Fox Option gain sits below the operating line. Flutter is required to mark the Fox Corporation option on FanDuel equity to fair value each quarter, in Q1 that adjustment added $293M to the bottom line without a single dollar changing hands. Remove that, account for interest expense that nearly doubled YoY from $85M to $156M, and the underlying business generated $79M in operating profit on $4.3B in revenue. Adjusted EBITDA grew just 2% to $631M with margin compressing 210 basis points to 14.7%. US adjusted EBITDA fell 26% to $119M as sportsbook revenue grew just 1% and handle declined 9%. Flutter trimmed full year guidance to $18.305B in revenue and $2.865B in adjusted EBITDA.

Total debt stands at $11.965B against cash of $1.512B, putting net debt at roughly $10.5B. Management expects leverage to increase further in Q2 and Q3 before reducing in Q4. The bull case requires revenue growth to continue outpacing interest expense throughout that period, given interest costs already nearly doubled in a single year.

The FanDuel CEO departure deserves highlighting most of all. Amy Howe had led FanDuel since 2021, guiding it through the period of rapid US market expansion that made it the number one sportsbook by market share. Her exit was announced the same day as a guidance cut, a handle decline, and a 26% drop in US adjusted EBITDA. Christian Genetski, previously FanDuel's president, has taken over day-to-day leadership.

US market share is the structural concern beneath the earnings report. FanDuel remains the leader, but DraftKings grew sportsbook revenue 24.1% in Q1 while Flutter's US sportsbook grew just 1%. One bad NFL season is just noise, but US sportsbook average monthly players declining 6% year-over-year is a less comfortable data point.

Regulatory risk is always present in this sector. Any adverse development around parlays or in-play betting, which drive a disproportionate share of margin, would hit the thesis directly.

My View

We have a beaten-down stock with a clear narrative for why it's down. A billionaire with over 27% of the company, accumulated almost entirely in the past thirteen weeks. Three additional institutional investors increasing exposure simultaneously. Six insiders buying in the open market in the same week. A $5B buyback program that has already returned $1.31B to shareholders and a business where the one-off headwinds; the NFL season, a UK tax hit and the elevated investment costs are now behind it.

None of that guarantees a recovery. The people with the most information and the most to lose from being wrong are not behaving like people who think this is a broken business.

I'm a buyer here, sized for the debt risk. Not a name to be overweight at 3.7x leverage in an uncertain macro environment, but at current prices with the conviction signals where they are, the risk/reward tilts long for me. Additionally, $FLUT trades at a forward EV/EBITDA of 9.63x versus DraftKings at 15.21x which is a decent discount for the market leader.

The next meaningful data point is Q2 earnings on 6th August. Watch for US handle growth, any commentary on FanDuel under its new leadership, and the leverage trajectory. The LSE delisting decision, due by end of June, will also tell you something about how management is thinking about the business long term. A clean exit from London and a full focus on the NYSE investor base is the move of a company that believes its future is American.

Ticker Thoughts is independent analysis. Current position held in $FLUT is 400 shares at $96.56 average.